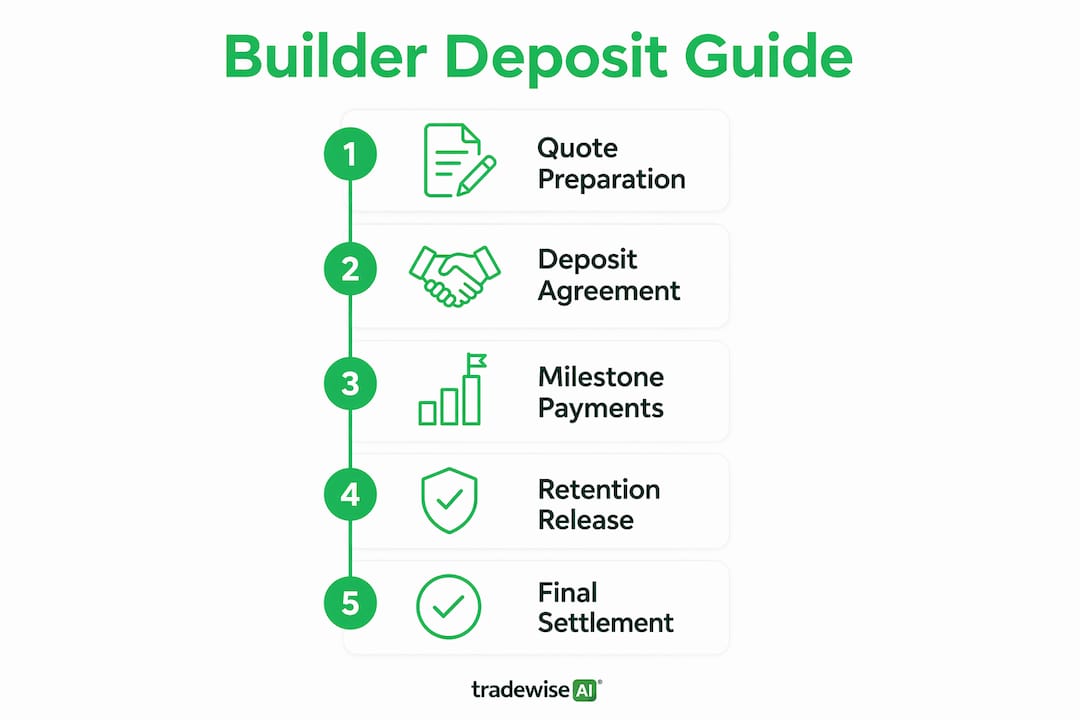

A builder job deposit policy is a formal agreement that defines how much a client pays upfront before work begins, under what conditions that money is held, and how it links to the project's payment schedule. Getting this right protects your cash flow, satisfies the Consumer Rights Act 2015, and removes the most common trigger for client disputes. The Construction Act 1996 adds further weight by requiring clear, written payment terms on most construction contracts. Without a properly structured deposit policy, you expose yourself to refund claims, delayed payments, and reputational damage that no amount of good workmanship can repair.

What are the standard deposit amounts for builder jobs?

Standard UK builder deposits sit at 10–20% of the total contract value for most residential projects. Bespoke or material-heavy jobs, such as timber-frame extensions or high-specification kitchen fits, can justify 25–40% where upfront material procurement is significant. Small, quick jobs under £1,000 typically require no deposit or a token 0–10% to cover call-out costs.

The table below shows typical deposit ranges by project type.

| Project type | Typical deposit range |

|---|---|

| Minor repairs and small jobs | 0–10% |

| Bathroom or kitchen renovation | 15–25% |

| Standard house extension | 10–20% |

| Large new build or bespoke project | 25–40% |

| Loft conversion (material-heavy) | 20–30% |

Charging above 25% for general work without a clear material or mobilisation justification is a recognised red flag for clients and can be challenged under unfair contract terms legislation. That threshold matters because it is the point at which a deposit shifts from a reasonable advance to something that looks like a cash grab.

Pro Tip: Always itemise what the deposit covers. Write "£2,400 deposit: £1,800 for structural timber, £600 for site mobilisation" rather than simply "25% deposit." Clients accept deposits far more readily when they can see exactly where their money goes.

Deposits function as cash flow tools, not income. Describing deposits as advances on materials or mobilisation costs in your contract language prevents the most common misunderstanding builders face: clients who assume the deposit is refundable if they change their mind after materials have been ordered.

How do UK regulations govern builder deposit policies?

The Consumer Rights Act 2015 defines an unfair contract term as one that creates a significant imbalance between the parties' rights and obligations to the detriment of the consumer. A deposit clause that is vague, disproportionate, or buried in small print falls squarely into that category. Courts have set aside deposit clauses on exactly these grounds, leaving builders with no legal claim to the money they have already spent.

The Construction Act 1996 requires that every construction contract includes an adequate mechanism for determining what payments are due, when they are due, and a final date for payment. This applies to most contracts with a value above a minimal threshold. Ignoring it does not make the requirement disappear. It simply means the Act's default payment terms apply instead of yours, which are rarely in your favour.

To keep your deposit policy legally sound, apply these principles:

- Write every deposit into a signed contract. Deposits requested by email without a signed agreement expose you to legal and reputational risk. A signed document is your primary defence.

- Link the deposit to a specific deliverable. State that the deposit covers material procurement or site mobilisation, not simply "commencement of works."

- Define what happens if the client cancels. Specify whether the deposit is non-refundable once materials are ordered, and under what conditions a partial refund applies.

- Reference the payment schedule explicitly. The contract should state the deposit amount, the trigger for each subsequent payment, and the final retention release date.

- Use plain language. The Consumer Rights Act 2015 requires that terms are transparent and expressed in plain, intelligible language. Legal jargon does not protect you. It undermines you.

For a deeper look at how contract types affect your deposit terms, the guide on UK construction contracts covers JCT, RIBA, and bespoke agreements in practical detail.

How should deposits link to project milestones?

Milestone-linked payments tied to building control inspections reduce payment disputes significantly compared to time-based payment schedules. The reason is simple: a milestone is objective. Either the foundations have passed inspection or they have not. A time-based payment, by contrast, invites arguments about whether enough progress has been made.

A typical UK payment schedule for a house extension looks like this:

| Stage | Trigger | Typical % of contract |

|---|---|---|

| Deposit | Contract signing | 10–20% |

| Foundations | Building control sign-off | 15–20% |

| Roof structure complete | Frame inspection passed | 20–25% |

| First fix (plumbing, electrics) | Completion of first fix | 15–20% |

| Second fix and plastering | Completion of second fix | 10–15% |

| Practical completion | Client sign-off on snagging | Remainder less retention |

| Retention release | End of defects liability period | 2.5–5% |

Professional contracts hold back 2.5–5% retention until 6–12 months after practical completion to cover any defects that emerge. This is standard in JCT and RIBA contracts. Retention is not a punishment. It is a structured incentive that motivates builders to return promptly for snagging, which in turn protects their reputation and referral pipeline.

Pro Tip: Tie every milestone payment to a building control inspection or a written client sign-off, not to your own assessment of completion. Third-party sign-off removes subjectivity and gives both sides a clear, agreed trigger for releasing funds.

The typical UK payment schedule runs from deposit at contract signing through to retention release after the defects liability period. Builders who follow this structure report fewer conflicts and faster final payments than those who invoice ad hoc.

Practical steps to implement a solid deposit policy

A deposit policy only works if it is written down, explained clearly, and enforced consistently. Follow these steps to build one that holds up legally and commercially.

-

Draft a contract clause for every job, regardless of size. Even a £500 bathroom repair deserves a one-page written agreement. State the deposit amount, what it covers, and the payment schedule for the remainder.

-

Provide an itemised deposit breakdown. List material costs, mobilisation fees, and any design or survey costs separately. Itemised deposit breakdowns are your best defence against unfair term claims.

-

Accept deposits by bank transfer or credit card only. Cash deposits leave no paper trail. A bank transfer creates a timestamped record that is admissible in any dispute. Credit card payments also give clients statutory protection, which reduces their anxiety about paying upfront.

-

State your cancellation and refund policy explicitly. Write something like: "The deposit is non-refundable once materials have been ordered. If the client cancels before material procurement, a full refund will be issued within 14 days." Ambiguity here is where disputes begin.

-

Keep a complete communications record. Save every email, text, and WhatsApp message related to the deposit and payment schedule. If a client later claims they were not told about the non-refundable nature of the deposit, your message history is your evidence.

-

Review your policy annually. Construction costs, material lead times, and legal standards change. A deposit policy written in 2023 may not reflect 2026 norms or updated Consumer Rights Act guidance.

For guidance on building accurate quotes that integrate your deposit structure from the start, the article on quoting building work covers pricing methodology in practical terms.

Common mistakes that lead to deposit disputes

Most deposit disputes are avoidable. They stem from a small set of recurring errors that builders make, often under time pressure or because they trust a client relationship that has not yet been tested.

- Demanding above-norm deposits without explanation. Asking for 40% upfront on a standard extension, without explaining the material costs behind it, signals inexperience or bad faith to clients. Justify every percentage point in writing.

- Failing to define project completion. Contracts must clearly define milestone completion, for example "after building control sign-off," not "when the builder considers the stage done." Vague definitions are the single most common cause of final payment refusals.

- Accepting cash without a receipt. Cash deposits are untraceable. If a client later denies paying, you have no record. Always issue a written receipt, even for cash, and follow up with a confirmation email.

- Omitting retention clauses. Skipping retention might feel client-friendly in the short term. In practice, it removes your leverage to return for snagging and leaves you exposed to warranty claims with no financial buffer.

- Ignoring scope creep in the payment schedule. When the client adds work mid-project, the original payment schedule becomes inaccurate. Issue a written variation order and update the payment schedule before the additional work begins.

Poor communication over payment schedule changes is the fastest way to turn a satisfied client into a disputing one. Address changes in writing, every time, without exception.

Key takeaways

A legally compliant builder deposit policy links every payment to a defined milestone, is written into a signed contract, and stays within the thresholds set by the Consumer Rights Act 2015.

| Point | Details |

|---|---|

| Standard deposit range | Keep deposits at 10–20% for most jobs; justify anything above 25% with itemised material costs. |

| Legal compliance | Every deposit must appear in a signed contract with plain-language terms under the Consumer Rights Act 2015. |

| Milestone-linked payments | Tie each stage payment to a building control inspection or written client sign-off to prevent disputes. |

| Retention clause | Hold back 2.5–5% until the defects liability period ends to cover snagging and protect your reputation. |

| Documentation | Itemised breakdowns and signed agreements are your primary defence against unfair term claims. |

Why fair deposit policies build better businesses

I have seen builders lose good clients not because of poor workmanship, but because of a poorly worded deposit clause. The client felt trapped, the builder felt accused, and a relationship that should have generated referrals ended in a Small Claims Court filing instead.

The builders I respect most treat their deposit policy the same way they treat their tools: maintained, fit for purpose, and never improvised on site. They send a signed contract before they lift a single brick. They explain the retention clause at the quote stage, not after practical completion. They describe the deposit as what it is, an advance on materials, not a booking fee.

There is a psychological dimension here that most guides ignore. When a client signs a contract that clearly shows a 2.5% retention being released after a 6-month defects period, they feel protected. That feeling of protection is what generates the five-star review and the referral to a neighbour. Transparency is not just a legal obligation. It is a commercial advantage.

My honest advice: stop treating your deposit policy as a financial instrument and start treating it as a trust-building document. The builders who will thrive in 2026 are the ones whose clients never have to wonder what happens to their money.

— Mateusz

How Tradewisehq helps builders manage deposits and payments

Running a deposit policy manually, across spreadsheets, email threads, and paper contracts, creates the exact gaps that disputes exploit.

Tradewisehq is an AI-powered operating system built for tradespeople. It lets you create itemised quotes with deposit breakdowns, generate signed contracts, and track milestone payments in one place. When a stage payment becomes due, the platform flags it automatically. When a client signs off a milestone, the record is timestamped and stored. You spend less time chasing paperwork and more time on site. For builders who want their deposit policy to work as hard as they do, Tradewisehq removes the admin burden and keeps every payment legally documented from day one.

FAQ

What is a fair deposit percentage for a UK builder?

A fair deposit for most UK building jobs sits at 10–20% of the contract value. Material-heavy or bespoke projects can justify up to 25–40%, provided the deposit is itemised and linked to specific procurement costs.

Are builder deposits refundable under UK law?

Deposits are not automatically refundable. Under the Consumer Rights Act 2015, a non-refundable deposit is lawful if it represents a genuine pre-estimate of loss or advance payment for materials, and if the terms are clearly stated in a signed contract.

What does the Construction Act 1996 require for payment terms?

The Construction Act 1996 requires every construction contract to include a clear mechanism for determining payment amounts, due dates, and a final payment date. Contracts that omit these terms are subject to the Act's default payment provisions.

How does milestone-linked payment reduce disputes?

Milestone-linked payments use objective triggers, such as building control sign-off, to release funds. This removes subjective arguments about whether work is complete and gives both parties a clear, agreed standard.

What is a retention clause and why does it matter?

A retention clause withholds 2.5–5% of the contract value until the end of the defects liability period, typically 6–12 months after practical completion. It protects clients against unresolved snagging and gives builders a financial incentive to return promptly.